Taxes for Expats review: The complete 2026 guide for Americans living in the UK

By Guest Writer • Published: 25 May 2026 • 11:32 • 5 minutes read

Image: Shutterstock.com

Living in the United Kingdom as a US citizen puts you inside two of the most robust and demanding tax systems in the world at the same time. HMRC expects a return if you are self-employed, own rental property, or earn above certain thresholds. The IRS expects a return on worldwide income, no matter what. For the growing number of Americans settled in Britain, that dual obligation is not a technicality to be ignored. It is an annual reality with real financial consequences if handled poorly.

Taxes for Expats (TFX) is a US expat-only tax preparation firm with more than 25 years of experience helping Americans navigate exactly this situation. Their UK-specific guide and services address the full complexity of US-UK cross-border filing, from the Foreign Tax Credit and FEIE election to FBAR reporting, pension treatment, and ISA complications. This review draws on that guide alongside broader 2026 expat tax data to give you a clear picture of what TFX offers and whether it is worth it for Americans living in Britain.

The US-UK tax overlap explained

The fundamental challenge is structural: the US taxes based on citizenship, the UK taxes based on residency. That means most Americans living in the UK file two separate returns, in two different currencies, under two different tax year calendars. The UK tax year runs from 6 April to 5 April, while the US calendar year runs from January to December.

The good news is that the US-UK tax treaty exists specifically to prevent double taxation on the same income. In practice, most Americans in the UK use the Foreign Tax Credit (Form 1116) to offset their US tax bill with taxes already paid to HMRC because UK tax rates are generally high enough to eliminate or significantly reduce the residual US liability. The Foreign Earned Income Exclusion remains available but is often less advantageous in the UK context, and the two cannot be applied to the same income simultaneously.

The 2026 tax landscape has added a few new wrinkles. From 6 April 2026, UK dividend tax rates have risen by two percentage points, meaning basic-rate taxpayers now face 10.75% on dividends and higher-rate taxpayers face 35.75%. A further increase on savings interest and rental income is scheduled for April 2027. For Americans in the UK with investment portfolios or rental property, these changes affect both the UK and US sides of the return.

Key UK-specific filing issues for US expats

Several issues come up consistently for Americans living in Britain that require specialist handling rather than a generic tax software approach.

ISAs are not tax-exempt for US purposes

One of the most common surprises for Americans in the UK is that Individual Savings Accounts, which are entirely tax-free under UK law, are not recognized as tax-exempt by the IRS. Dividends and interest earned inside a UK ISA must still be reported on the US return, and the account itself may need to be reported under FATCA depending on the balance.

Pension treatment requires careful handling

UK workplace pensions and the State Pension interact with the US-UK tax treaty, but the specific treatment depends on who the employer is and what type of pension is involved. Government service pensions are typically only taxable in the UK under the treaty. Private employer pensions and self-invested personal pensions (SIPPs) may be treated differently. Getting this wrong on either return can create overclaims or missed credits.

FBAR and FATCA for UK accounts

FBAR (FinCEN Form 114) is required for any US person whose combined foreign bank accounts current accounts, savings accounts, brokerage accounts, and certain other financial accounts exceed $10,000 at any point during the calendar year. FATCA reporting (Form 8938) applies when specified foreign financial assets exceed higher thresholds that vary by filing status and residency. UK bank accounts, investment accounts, and pensions may all count toward these thresholds.

Self-employment and National Insurance

Americans in the UK who are self-employed pay both UK National Insurance and may owe US self-employment tax on the same earnings. The US-UK totalization agreement can help avoid this double charge, but it requires correctly applying the agreement and documenting your coverage under one system rather than two.

What TFX offers Americans in the UK

TFX operates as a fully remote, expat-only preparation service accessible from anywhere in the world. For Americans in the UK, that means a process that works around UK time zones and does not require a visit to a US-facing office. The intake questionnaire, document portal, and communication all run through an encrypted online system (AES-256, two-factor authentication).

Their preparers are CPAs and Enrolled Agents with at least ten years of expat-specific experience, and every return passes through a dual review before the client sees it. For UK-based filings that may involve pension treaty positions, ISA reporting complications, FBAR obligations, and FTC optimization, that expertise level is relevant these are not situations where a junior preparer following a checklist produces a reliable outcome.

TFX does not provide UK Self Assessment preparation, which is worth noting clearly. If you also need to file with HMRC because you are self-employed, have rental income, or HMRC has specifically requested it you would need a separate UK accountant alongside TFX’s US service.

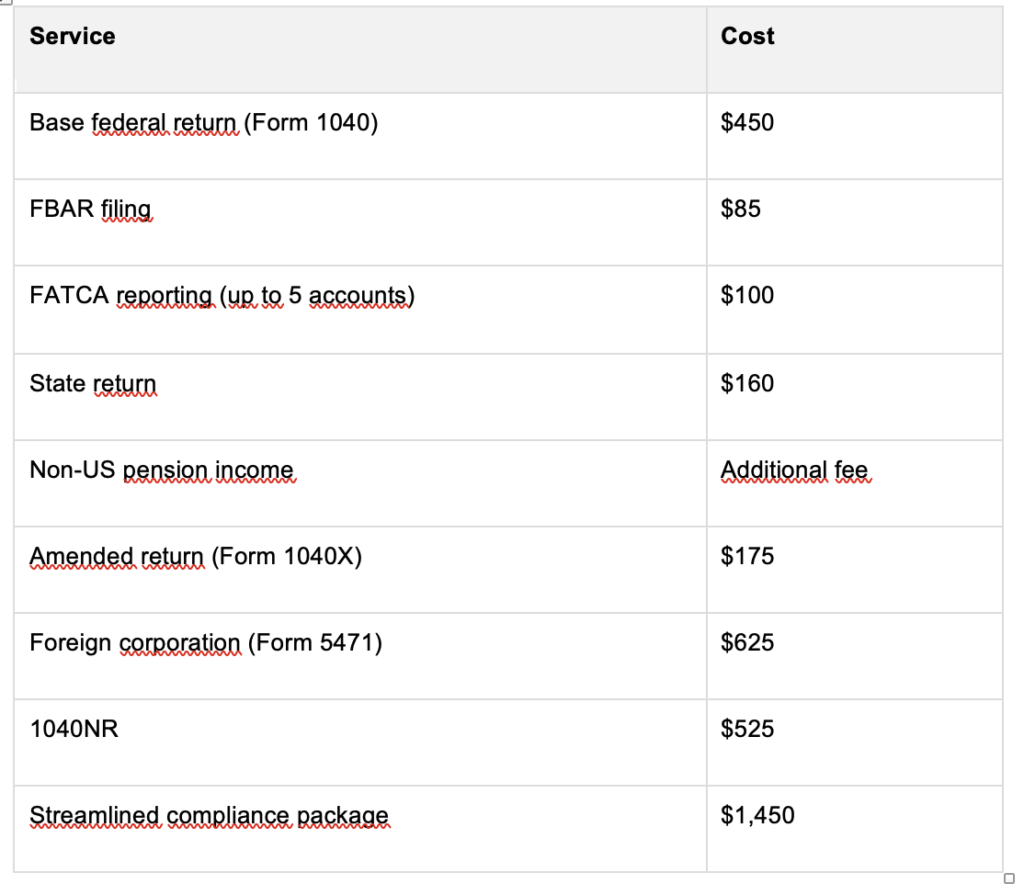

2026 pricing for US expats in the UK

All TFX fees are in USD with no VAT, which is a relevant point for UK-based clients comparing against British accountants who quote in sterling and charge VAT on top.

For a typical American professional in the UK employed, with a UK bank account, a workplace pension, and perhaps a UK investment account the base return plus FBAR and possibly FATCA would typically place the total somewhere between $535 and $635, before any additional forms for pension treatment or other complexity.

The streamlined package is available for Americans who have not been filing correctly. For UK-based expats who were unaware of their US filing obligation a common situation the Streamlined Foreign Offshore Procedures offer a penalty-free path to catch up, and TFX packages this at $1,450 for three years of returns and six years of FBAR.

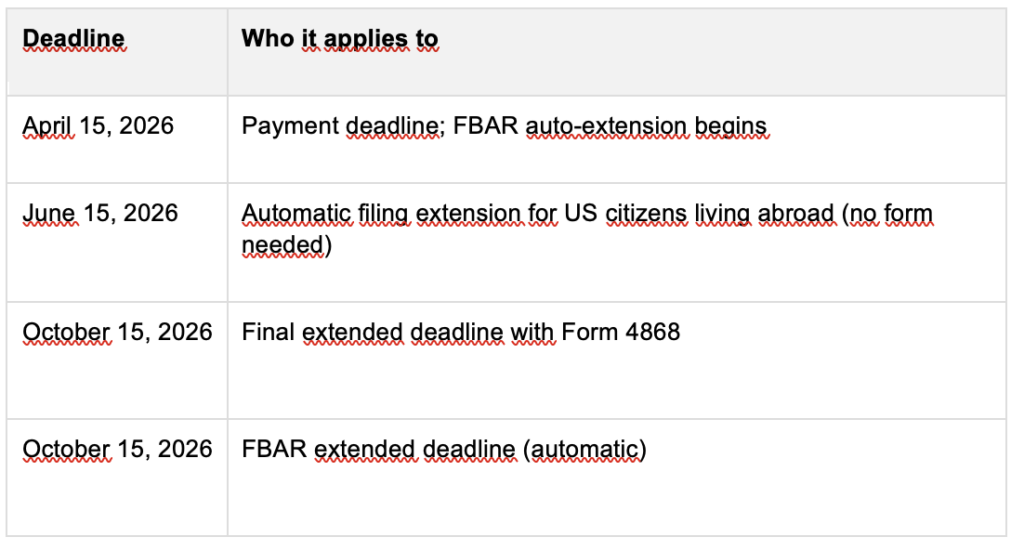

Key 2026 filing deadlines

Even with the June 15 extension, any taxes owed still accrue interest from April 15. Filing the return and paying what is owed as early as possible reduces that cost.

Is TFX the right choice for Americans in the UK?

TFX is well-positioned for Americans in the UK who have more than a simple return. That includes:

- Professionals with UK employment income, workplace pensions, and UK bank accounts requiring FBAR

- Self-employed individuals who need a US self-employment tax analysis alongside FTC optimization

- Investors with UK ISAs, brokerage accounts, or dividend income affected by 2026 UK rate changes

- Retirees drawing UK State Pension or private pension alongside US Social Security

- Expats who have not been filing and need a structured catch-up path

For Americans in the UK whose situation is very straightforward one UK employer, no foreign accounts above $10,000, no investments, no pension complexity cheaper options may be sufficient. But that description covers relatively few Americans who have been in the UK for more than a year or two.

For everyone else, the combination of specialist expertise, transparent pricing, remote-first process, and dual-review quality control makes TFX a practical and credible choice for US tax compliance from the UK.

Practical steps before you start

- Pull together all UK financial accounts and check whether their combined balance may exceed the $10,000 FBAR threshold at any point during the year

- Identify all pension arrangements: UK workplace pension, SIPP, State Pension and note the employer type, as this affects treaty treatment

- Gather P60s, P45s, and any HMRC Self Assessment documents you have filed, as these feed into the US return preparation process

- Note any UK ISA holdings and understand that income generated inside them will still need to be reported to the IRS

- Check whether any new UK dividend or investment income changes from April 2026 affect your expected US tax position before the next filing season

Handled well, the US-UK tax overlap is manageable. Handled by someone unfamiliar with the specifics, it is a recurring source of errors, missed credits, and unnecessary costs. TFX’s UK-specific expertise addresses that gap directly.

Follow Euro Weekly News on Google News

Get breaking news from Spain, travel updates, and expat stories directly on your Google News feed.

Follow on Google NewsSign up for personalised news

Subscribe to our Euro Weekly News alerts to get the latest stories into your inbox!

By signing up, you will create a Euro Weekly News account if you don't already have one. Review our Privacy Policy for more information about our privacy practices.

Guest Writer

Comments