The monthly payment trap: Why cheap per month can cost you more

By Guest Writer • Published: 21 Apr 2026 • 16:09 • 8 minutes read

Image: Shutterstock

If you have ever walked into a dealership and heard the words “only £299 a month”, you already know how powerful that number can be. It sounds affordable. It sounds sensible. And for most people, it immediately feels more manageable than staring at a £20,000 price tag.

Before comparing deals, using a car finance calculator to check how deposit, term length, and interest affect the total can make that monthly figure far less misleading.

That is exactly why finance deals are marketed this way. Dealers and lenders know that buyers focus on the monthly figure, not the total. It is much easier to say yes to £299 than to £24,000.

The scale of this is significant. Over 2 million cars were bought using motor finance at the point of sale in the UK in 2024 alone, and motor finance now accounts for more than 80% of all private new car sales. Most of those buyers were shown a monthly payment figure before they were shown anything else.

That monthly number is not wrong, exactly. But it only tells you part of the story. The rest of the story is where the real cost hides.

The real cost hidden behind that monthly figure

When a lender sets your monthly payment, they are not doing you a favour by making it smaller. They are rearranging the money you owe in a way that works for them and often costs you more.

There are three main things that quietly push up your total bill, even when your monthly payment looks low.

The first is the interest rate, or APR. This is the annual percentage rate charged on the money you borrow. A deal with an 8% APR versus a 12% APR might only change your monthly payment by £20 to £30, but over a three or four year agreement, the difference in total interest paid can run into hundreds of pounds.

The second is the loan term. Spreading the same loan over 60 months instead of 36 months will reduce your monthly payment noticeably. But you will pay interest for an extra two years, which means you pay significantly more in total. It is like asking for a smaller slice of cake, only to find you end up eating more cake overall.

The third, and the one most buyers miss completely, is the balloon payment on a PCP deal. On a £25,000 car with a £2,500 deposit, a PCP deal might give you a monthly payment of around £380. The equivalent HP deal on the same car would be roughly £690 a month. The PCP looks like the obvious choice. But at the end of a PCP deal, there is often a large lump sum, sometimes £8,000 to £15,000, sitting there if you want to actually keep the car. You have been paying interest on that amount the whole time without reducing it.

The monthly payment tells you what comes out of your account each month. The total amount payable tells you what the car actually costs you. Always ask for both before you sign.

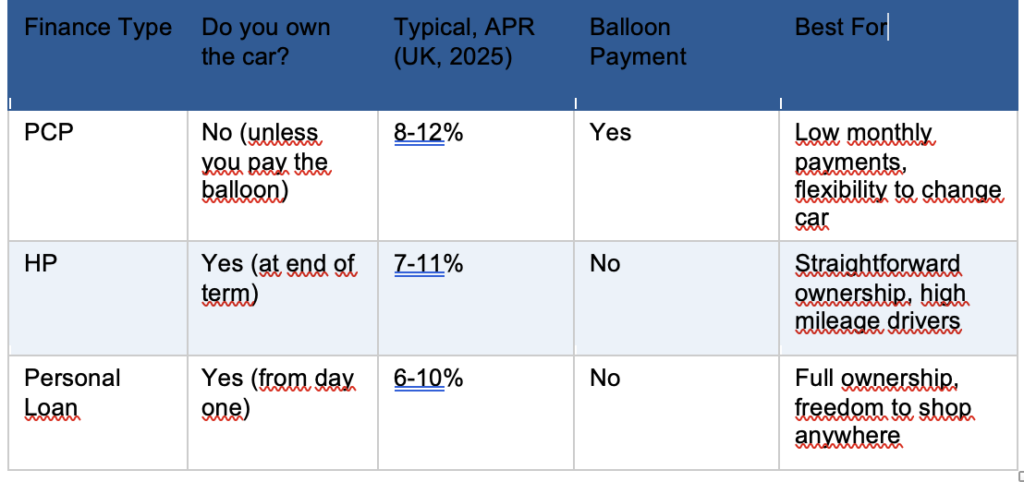

PCP vs HP vs Personal Loan: What you are actually signing up for

Most UK buyers end up choosing between three options: PCP, HP, or a personal loan. Here is how they compare at a glance.

PCP, or Personal Contract Purchase, is the most widely used option in the UK. Your monthly payments are lower because you are only paying off the amount the car is expected to lose in value during your agreement, not its full price. At the end, you can hand the car back, pay a lump sum to keep it, or use any remaining value as a deposit on your next deal.

HP, or Hire Purchase, is more straightforward. You borrow the full cost of the car and pay it off in equal monthly instalments. Once you make the last payment, the car is yours. There are no mileage limits, no balloon payment, and no end-of-term decisions.

A personal loan gives you the money upfront to buy the car outright, which means you own it from day one. If you have a good credit score, you can sometimes find personal loan rates that are lower than what a dealership will offer you on finance, and you are free to buy from any seller, not just one who has a finance arrangement in place.

How stretching the term costs you more

One of the most common ways buyers accidentally pay too much is by simply agreeing to a longer finance term to get the monthly payment down to a comfortable level.

Here is a simple example. Say you are borrowing £15,000 at 9% APR.

Over 36 months, your monthly payment would be around £477. The total amount you repay is approximately £17,172.

Over 60 months, your monthly payment drops to around £311. That feels much more manageable. But the total you repay climbs to approximately £18,660.

That is a difference of nearly £1,500 for the exact same car, on the exact same interest rate, just by choosing a longer term.

Now consider that many PCP and HP deals run to 48 or even 60 months. The monthly saving can feel meaningful in the moment, but the total cost comparison is what actually matters to your finances over time.

A good rule of thumb: try not to take a finance term that is longer than you expect to keep the car. If you are planning to change cars after three years, a five year HP deal leaves you in a difficult position, often still paying off a car you no longer own.

Always look at the total amount payable, not just the monthly figure. This one number tells you exactly how much the deal will cost you from start to finish.

The extras that quietly add up

The monthly payment and the total amount payable still do not tell the full story. There is a list of additional costs that regularly catch buyers off guard, particularly on PCP deals.

Before you sign anything, check whether any of these apply to your agreement:

- GAP insurance. This covers the difference between what your insurer pays out and what you still owe on finance if your car is written off. Dealers often add this at the point of sale and bundle it into the monthly payment. You can usually buy it separately for considerably less.

- The Optional Final Payment (balloon). On a PCP deal, this is the lump sum you would need to pay at the end if you want to keep the car. It can range from several thousand pounds to well over ten thousand depending on the car. You pay interest on this amount throughout the entire agreement without reducing it.

- Excess mileage charges. PCP agreements come with an agreed annual mileage limit, typically between 8,000 and 12,000 miles per year. If you go over it, you will be charged per mile at the end of the contract, usually between 5p and 15p per mile. Two thousand extra miles at 10p per mile adds £200 to your final bill.

- Wear and tear charges on return. If you hand the car back at the end of a PCP deal, the finance company will inspect it. Anything beyond what they consider fair wear and tear will be charged to you. Scratches, scuffs, and tyre wear can add up quickly.

- Early settlement fees. If you want to pay off the finance early, some agreements allow you to do this at a discount through a process called Voluntary Termination once you have paid off half the total. Others charge early repayment fees. Always check before you assume you can exit early without cost.

- Admin and arrangement fees. Some finance agreements carry a small fee at the start or end of the deal that adds to the total cost. These are often listed in the small print rather than highlighted in the headline numbers.

What the FCA scandal tells us about the industry

You may have heard about the ongoing car finance compensation story in the news. This is worth understanding, because it says something important about how the industry has worked.

For many years, car dealers could earn a commission from lenders simply by arranging finance for customers. In many cases, the higher the interest rate they set, the more commission they earned. Buyers were often not told this was happening.

The Financial Conduct Authority (FCA) has been reviewing tens of millions of motor finance agreements made between 2007 and 2024. The average expected payout is around £829 per affected agreement, and the total industry liability is estimated to run into billions of pounds. Anyone who hasn’t yet been contacted can still submit a claim until 31 August 2027.

This matters for anyone buying a car today because it is a reminder that the finance deal offered to you at a dealership is not necessarily the best deal available. The salesperson arranging your finance may have a financial incentive to put you on a particular product or a higher rate.

This is not universally the case, and regulations have tightened significantly since 2021. But it is a good reason to always compare options before accepting the first finance offer you are given.

If you took out car finance between 2007 and 2024, it may be worth checking whether you are owed compensation through the FCA scheme. The deadline to claim is 31 August 2027.

How to actually get a good deal (not just a low payment)

Getting a genuinely good car finance deal comes down to a few habits that most buyers skip because they feel complicated. They are not.

Start with the total amount payable, not the monthly figure. This is the number printed in every finance agreement and it tells you the true cost from start to finish. Compare this number across deals, not the monthly payment.

Compare the APR across lenders. The dealership is one source of finance. Banks, credit unions, and online lenders are others. Getting one or two quotes before you visit a showroom gives you something to compare against.

Know your total running costs. The average monthly cost of owning a car in the UK is £280 to £300, which includes fuel, insurance, and road tax. Your finance payment sits on top of that. Make sure you are budgeting for the whole picture, not just the monthly instalment.

Use an independent broker. A broker who is not tied to a single lender can compare deals across the market and explain the options in plain language. They are obligated to act in your interest, not the lender’s.

Be honest about your mileage. If you regularly cover 15,000 miles a year, do not agree to a PCP deal with a 10,000 mile limit to get a lower monthly payment. The excess mileage charges at the end will more than wipe out any saving.

Ask what happens at the end. Before you sign, know exactly what your options are when the agreement finishes. For a PCP deal, ask what the balloon payment is and how much the car is expected to be worth at that point.

The car finance market in the UK is large, competitive, and increasingly transparent. That means good deals do exist. But finding them requires looking past the monthly payment figure and understanding what you are actually agreeing to.

Take your time, compare the total costs, and never let a low monthly number be the reason you sign.

Sign up for personalised news

Subscribe to our Euro Weekly News alerts to get the latest stories into your inbox!

By signing up, you will create a Euro Weekly News account if you don't already have one. Review our Privacy Policy for more information about our privacy practices.

Guest Writer

Comments